Subscribe

SubscribeOn January 27, 2022, Supreme Court of the United States Justice Stephen Breyer formally announced his retirement, effective when the Supreme Court breaks for summer recess in June or July later this year—after his successor has been nominated and confirmed. Justice Breyer has served on the Supreme Court since 1994 and is the second-most senior justice after Justice Clarence Thomas.

Although Justice Breyer did not author a substantial number of tax opinions, the ones he did author are extremely important and include:

- Marinello v. United States (criminal tax fraud)

- United States v. Home Concrete & Supply, LLC (limitations period for assessing tax)

- United States v. Brockamp (limitations period for refund or credit claims).

This post focuses on the Home Concrete case.

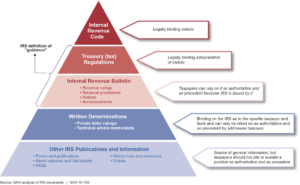

Home Concrete involved a challenge to the validity of US Department of the Treasury (Treasury) regulations issued during litigation that purported to overrule existing case law. In a 5-4 opinion authored by Justice Breyer, the Supreme Court rejected both the government’s statutory interpretation of the “substantial omission from gross income” exception to the normal three-year statute of limitations and the interpretation advanced in retroactive regulations issued during pending litigation. In doing so, the Court first applied principles of stare decisis and adhered to its prior opinion in Colony, Inc. v. Commissioner, which interpreted almost identical statutory language from the predecessor statute. It then held that, because it already interpreted the statute, there is no longer any different interpretation that is consistent with that precedent and available for adoption by the agency.

The history and procedural background are fascinating, and some of the issues highlighted in the case, but not directly decided, have been—and continue to be—developed. Further background on the case can be found in our 2012 Tax Executive article, “Home Concrete: The Story Behind the IRS’s Attempt to Overrule the Judiciary and Lessons for the Future.”

Practice Point: Home Concrete remains important today as there are several cases in the administrative and judicial pipeline involving challenges to tax reform and transfer pricing regulations. It is a must-read for any taxpayers who are currently, or are considering in the future, challenging the validity of Treasury regulations.

Andrew Roberson was one of the lawyers representing Home Concrete before the Supreme Court.

read more

")