Oftentimes, taxpayers rely on various authorities in planning transactions and reporting them for tax purposes, as well as defending them during an Internal Revenue Service (IRS) audit, appeals or in litigation. These sources include authorities like the Internal Revenue Code, legislative history and other legislative materials, Treasury regulations and other IRS published guidance (e.g., revenue rulings, revenue procedures, notices, announcements), IRS private guidance (e.g., chief counsel advice, technical advice memoranda, private letter rulings, etc.), and case law. As we have discussed previously, these authorities are afforded different weight by courts and the IRS, and can serve different purposes in your matter.

On June 20, 2017, the Internal Revenue Service (IRS) Large Business and International Division (LB&I) hosted its final webinar regarding LB&I Campaigns. Our previous coverage of LB&I Campaigns can be found here. The webinar focused on two campaigns: (1) Section 48C Energy Credits and (2) Land Developers – Completed Contract Method.

In October 2016, the Internal Revenue Service (IRS) revised the Internal Revenue Manual (Manual) 8.6.1.4.4 to provide IRS Appeals Division (Appeals) with discretion to invite representatives from the IRS Examination Division (Exam) and IRS Office of Chief Counsel (Counsel) to the Appeals conference. Many tax practitioners opposed this change, believing that it undermines the independence of Appeals and may lead to a breakdown in the settlement process.

In May 2017, the American Bar Association (ABA) Section of Taxation submitted comments recommending the reinstatement of the long-standing Manual provision regarding the limited circumstances for attendance by representatives from Exam and Counsel at settlement conferences. Additionally, the Tax Section’s comments were critical of the practice whereby some Appeals Team Case Leaders (ATCLs) in traditional Appeals cases are “strongly encouraging” IRS Exam and the taxpayer to conduct settlement negotiations similar to Rapid Appeals or Fast Track Settlement, such that many taxpayers do not feel they can decline such overtures. The Tax Section comments suggested that the use of Rapid Appeals Process and Fast Track Settlement should be a voluntary decision of both the taxpayer and IRS Exam and the use of these processes should be the exception rather than the rule. (more…)

On Tuesday, May 23, 2017, the Internal Revenue Service (IRS) Large Business and International Division (LB&I) hosted its sixth in a series of eight webinars regarding LB&I Campaigns. Our previous coverage of LB&I Campaigns can be found here. The webinar focused on two cross-border activities campaigns: (1) the Repatriation Campaign and (2) the Form 1120-F Non-Filer Campaign. Below, we summarize LB&I’s comments on the new campaigns.

Repatriation Campaign

In general, the active earnings of foreign subsidiaries are not subject to tax until repatriated to the United States. Typically, those repatriations would be treated as dividends and would be subject to tax. LB&I stated that, through examination experience, it has observed that some taxpayers have engaged in techniques to permit repatriation from such entities while inappropriately avoiding US taxation.

LB&I developed the Repatriation Campaign with three goals in mind. First, LB&I was concerned with developing better objective techniques to identify risks across the broad taxpayer population. Second, LB&I is trying to improve sightlines into a broader segment of the LB&I population beyond the largest taxpayers under continuous audit. Third, LB&I intends to address any compliance risks related to repatriation in a way that increases voluntary compliance.

Unlike other campaigns, LB&I is not focused on a specific structure or techniques. LB&I is instead trying to identify objective indicators of opportunities to implement questionable planning (in the IRS’s view). Per LB&I, returns with those indicators are more likely to present compliance risks and are more likely to be selected. LB&I stated that it does not believe publicly identifying those indicators will increase voluntary compliance. Historically, when LB&I selected a return for examination, it did not necessarily start with any particular issue; any issue could be examined. If a return is selected under this campaign, LB&I’s initial focus will be narrower, but other compliance issues, if discovered, can still be added to the audit. Repatriation issues can also be raised outside of the Repatriation Campaign—possibly in a continuous audit or in an audit relating to another LB&I campaign. (more…)

On Wednesday, May 10, 2017, the Internal Revenue Service (IRS) Large Business and International Division (LB&I) hosted a webinar with the Association of International Certified Professional Accountants (AICPA) regarding LB&I’s recently-announced campaigns targeting inbound distributors and taxpayers who either were declined by, or withdrew from, the IRS’s Offshore Voluntary Disclosure Program (OVDP). Our previous coverage of LB&I’s campaign initiatives can be found here. The slides from the presentation are available here.

Inbound Distributors

As described by the IRS, this campaign is intended to address transfer pricing in the context of United States distributors of goods sourced from foreign-related parties that may have reported gains or losses that are not commensurate with the functions performed and the risk assumed.

As discussed in Wednesday’s webinar, this campaign is somewhat unique in that the IRS is still evaluating whether this issue presents an actual—rather than a mere potential—threat of noncompliance. The IRS has identified a series of returns to be sent into the field for examination, but is currently holding them to evaluate whether a genuine threat of noncompliance exists. The IRS also stated that the campaign is being designed to allow for flexibility to release returns quickly, if compliance can be readily ascertained. (more…)

We previously wrote two blog posts about the 2nd International Conference on Taxpayer Rights held in Vienna, Austria in March 2017 hereand here. Videos of each panel discussion are now available for viewing here. Planning is currently underway for the 3rd International Conference on Taxpayer Rights, which will be held in The Netherlands on May 3-4.

A frequently disputed tax issue is the proper treatment of costs incurred by taxpayers and whether they are currently deductible or must be capitalized. Internal Revenue Code (Code) Section 162 generally provides a deduction for ordinary and necessary business expenses paid or incurred during the taxable year in carrying on any trade or business. However, Code Section 263 provides no deduction for any amount paid for permanent improvements made to increase the value of any property. Code Section 263 requires capitalization of, amongst other things, costs paid or incurred to facilitate the acquisition of a trade or business. The capitalization rules of Code Section 263 trump the deductibility rules of Code Section 162. (more…)

Internal Revenue Code Section 199 permits taxpayers to claim a 9 percent deduction related to the costs to develop software within the U.S. The relevant regulations and their interpretation, however, place substantial restrictions on claiming the benefit.

Moreover, the regulations and the government’s position haven’t kept up with the technological advances in computer software.

Before claiming the deduction on your return, consider that the Internal Revenue Service has this issue within its sights, and perhaps it will be the subject of one of their new “campaigns.”

In 2004, Congress enacted I.R.C. Section 199 to tip the scales of global competitiveness more in favor of American business. The main motivation of the statute was to create jobs by encouraging businesses to manufacture and produce their products in the U.S. The tax benefit, however, isn’t available for services, a theme that pervades many of the provisions in the statute and regulations.

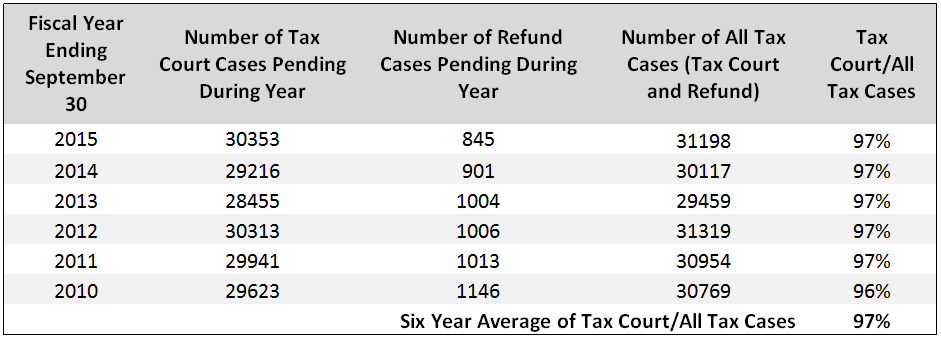

Taxpayers can choose whether to litigate tax disputes with the Internal Revenue Service (IRS) in the US Tax Court (Tax Court), federal district court or the Court of Federal Claims. Claims brought in federal district court and the Court of Federal Claims are tax refund litigation: the taxpayer must first pay the tax, file a claim for refund, and file a complaint against the United States if the claim is not allowed. Claims brought in the Tax Court are deficiency cases: the taxpayer can file a petition against the IRS Commissioner after receiving a notice of deficiency and does not need to pay the tax beforehand.

As demonstrated in the chart below, approximately 97 percent of tax claims are instituted in the Tax Court. It should be noted that, after a taxpayer files a petition in Tax Court, the taxpayer no longer has the option of bringing the claim in any other court for the year(s) at issue.

On April 4, 2017, QinetiQ U.S. Holdings, Inc. petitioned the US Supreme Court to review the US Court of Appeals for the Fourth Circuit’s decision that the Administrative Procedure Act of 1946 (APA) does not apply to the Internal Revenue Service (IRS) Notices of Deficiency. We previously wrote about the case (QinetiQ U.S. Holdings, Inc. v. Commissioner, No. 15-2192) here, here, here and here. To refresh, the taxpayer had argued in the US Tax Court that the Notice of Deficiency issued by the IRS, which contained a one-sentence reason for the deficiency determination, violated the APA because it was “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” The APA provides a general rule that a reviewing court that is subject to the APA must hold unlawful and set aside an agency action unwarranted by the facts to the extent the facts are subject to trial de novo by the reviewing court. The Tax Court disagreed, emphasizing that it was well settled that the court is not subject to the APA and holding that the Notice of Deficiency adequately notified the taxpayer that a deficiency had been determined under relevant case law. The taxpayer appealed to the 4th Circuit, which ultimately affirmed the Tax Court’s decision. (more…)

Subscribe

Subscribe

")