Subscribe

SubscribePresented below is our summary of significant Internal Revenue Service (IRS) guidance and relevant tax matters for the week of February 4 – 8, 2019.

February 4, 2019: The IRS released final instructions for Form 1065, US Return of Partnership Income, incorporating changes made by the Tax Cuts and Jobs Act.

February 5, 2019: The IRS issued a news release postponing certain tax deadlines for taxpayers affected by the earthquake that occurred in Alaska on November 30, 2018.

February 6, 2019: The IRS released final instructions for Form 1041, US Income Tax Return for Estates and Trusts, and supporting schedules, incorporating changes made by the Tax Cuts and Jobs Act.

February 6, 2019: The IRS released final instructions for Form 8991, dealing with the base erosion and anti-abuse tax (BEAT) of section 59A of the Code, enacted as part of the Tax Cuts and Jobs Act.

February 7, 2019: The IRS issued a news release providing guidance on identifying and avoiding unethical tax return preparers.

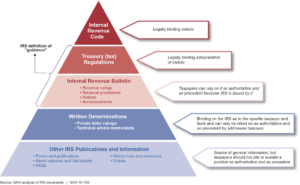

February 8, 2019: The IRS released its weekly list of written determinations (e.g., Private Letter Rulings, Technical Advice Memorandums and Chief Counsel Advice).

Special thanks to Le Chen in our DC office for this week’s roundup.

read more

")