Subscribe

SubscribePresented below is our summary of significant IRS guidance and relevant tax matters for the week of August 27 – 31, 2018:

August 27, 2018: The IRS announced changes to its Compliance Assurance Process (CAP) program. We posted about the changes to CAP here.

August 28, 2018: In Notice 2018-70, the IRS announced that it will issue proposed regulations clarifying the definition of a “qualifying relative” for various purposes, including the new $500 credit for certain dependents.

August 30, 2018: The Office of Management and Budget (OMB) completed its review of a proposal to remove parts of the Internal Revenue Code Section 385 regulations, which address the treatment of debt among members of an expanded affiliated group.

August 31, 2018: The IRS released Revenue Procedure 2018-58, which includes the current list of jurisdictions subject to reporting requirements for certain deposit interest paid to nonresident alien individuals.

August 31, 2018: The IRS published statistics regarding US source income payments to foreign persons reported on Form 1042-S.

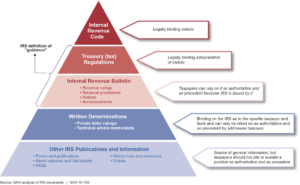

August 31, 2018: The IRS released its weekly list of written determinations (e.g., Private Letter Rulings, Technical Advice Memorandum and Chief Counsel Advice).

Special thanks to Kevin Hall in our DC office for this week’s roundup.

read more

")