The Internal Revenue Service (IRS) views convertible virtual currency as property, not foreign currency. As such, taxpayers must record and track the tax basis of each unit of virtual currency held in order to properly report taxable gain or loss when disposing of a unit or units of virtual currency. This article reviews the IRS’s position with respect to the identification and tax basis of such units.

Given limited guidance by US tax authorities regarding taxation of virtual currency activities, taxpayers with such holdings may find themselves in uncharted territory as to whether to take positions that are contrary to IRS pronouncements. This article explores relevant notices, rulings and FAQs, and reviews the types of deference that courts tend to put on different types of IRS interpretations and guidance.

In the wake of tax reform, taxpayers and practitioners alike are anxious for guidance and clarification on how the new laws impact transactions and reporting positions. The Internal Revenue Service (IRS) has previously stated that implementing tax reform is its highest priority, but that issuing guidance on the entire bill would likely take a substantial amount of time. Since December 2017, the IRS has published a host of notices, revenue procedures and administrative guidance. In some instances, the guidance was mechanical (e.g., Notice 2018-38), and in others it was more substantive (e.g., Notice 2018-28, Notice 2018-18, Rev. Proc. 2018-26).

On May 31, 2018, the IRS announced an “all hands on deck” effort to implement tax reform through 11 groups working closely with the Treasury Department. The IRS originally stated that it did not plan to release any more proposed regulations before the end of the year. Instead, it would issue tax Forms (with instructions) that would need to be filed by taxpayers before the end of the year. On June 7, 2018, the IRS explained that it does plan to issue proposed regulations “covering all major portions” of the bill starting in September and ending in December 2018 (the IRS specifically plans to finalize the temporary aggregation regulations by September to stop them from sunsetting). The IRS reported it is in “very good shape” to meet these deadlines. Additionally, at a recent American Bar Association Section of Taxation meeting, IRS international counsel acknowledged year-end financial reporting for global companies and stated that international tax regulations are intended to be released in the fall instead of the end of the year. Regulations under Internal Code Section 965 are planned for issuance this summer, and other areas of guidance include global intangible low-tax income, also known as the GILTI tax.

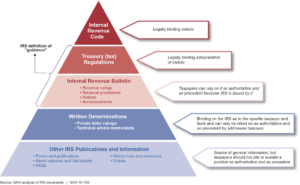

The United States Government Accountability Office (GAO) recently released a report regarding how the Internal Revenue Service (IRS) communicates tax guidance to the public.This report was prepared following bipartisan requests from members of both houses of Congress.

The GAO report: (1) analyzed documents that defined IRS guidance types; (2) reviewed the IRS’s policies and procedures for issuing guidance; (3) reviewed literature on the IRS’s issuance of guidance; (4) interviewed individuals at relevant government and tax practitioner organizations; and (5) reviewed IRS guidance issued during 2013 through 2015. Below is a chart included in the GAO report that illustrates various forms of guidance, and the weight that the IRS says attaches to each.

The GAO found that the IRS uses many different forms of guidance to communicate its interpretation of tax laws to the public, but considers only the Internal Revenue Bulletin (IRB) guidance to be authoritative. The IRS’s statement that only IRB guidance is authoritative could be considered an oversimplification. We previously wrote (here, here, and here) about how deference principles may apply to various forms of guidance.

The GAO found further that while the IRS has detailed procedures for identifying, prioritizing, and issuing new guidance, the IRS lacks procedures for documenting the decision about what form of guidance to issue.

As discussed in an earlier post, 3M Co. v. Commissioner, T.C. Dkt. No. 5816-13, involves 3M Company’s (3M) challenge to the Internal Revenue Service’s (IRS) determination that Brazilian legal restrictions on the payment of royalties from a subsidiary in that country to its US parent should not be taken into account in determining the arm’s-length royalty between 3M and its subsidiary under Treas. Reg. § 1.482-1(h)(2). The case has been submitted fully stipulated under Tax Court Rule 122. We discussed the parties’ opening briefs, filed on March 21, 2016, here. Reply briefs were filed on June 29, with the IRS filing an amended reply brief on August 18.

3M returns to its argument that Treas. Reg. § 1.482-1(h)(2) is “procedurally invalid” because Treasury and the IRS failed to satisfy the requirements of section 553 of the Administrative Procedure Act (the APA) when they promulgated the regulations. 3M notes that the IRS completely ignored this argument in its opening brief. Citing the Supreme Court’s recent opinion in Encino Motorcars, discussed in more detail here, 3M points out that Treasury and the IRS made significant changes to the regulation, but offered no explanation for the changes. This, 3M argues, renders the regulation invalid. 3M observes that compliance with the two-step Chevron test would not save a regulation that is procedurally invalid, noting that such compliance is “a necessary but not a sufficient condition for a regulation to be upheld.”

Global tax policy has evolved dramatically, with multinational corporations coming under attack from all directions. To respond to budget deficits and economic austerity, worldwide taxing authorities are deploying a new weapon: information exchange. As multinational corporations struggle to remain compliant and competitive in a world where effective tax rate management can be a critical element of cost control, what does this evolution mean for your business?

One group of six professors (Harvey Group) first notes its agreement with the arguments advanced by the government in its opening brief. In particular, the Harvey Group concurs with the argument that “coordinating amendments promulgated with Treas. Reg. § 1.482-7(d)(2) vitiate the Tax Court’s analysis in Xilinx that the cost-sharing regulation conflicts with the arm’s-length standard.” It then goes on to note its agreement with the government’s argument that “the ‘commensurate with the income’ standard … contemplates a purely internal approach to allocating income from intangibles to related parties.”

Having thus supported the government’s commensurate-with income-based arguments, the Harvey Group argues that the regulation in question is, in any event, consistent with the general arm’s-length standard of Code Section 482. It does so based principally on the proposition that “[s]tock-based compensation costs are real costs, and no profit-maximizing economic actor would ignore them.” However, that said, “there are material differences between controlled and uncontrolled parties’ attitudes, motivations and behaviors regarding stock-based compensation.” Thus, according to the Harvey Group, the Tax Court erred when it concluded that “Treasury necessarily decided an empirical question when it concluded that the final rule was consistent with the arm’s-length standard,” because “[n]o empirical finding that uncontrolled parties do, or might, share stock-based compensation costs is required to support Treasury’s regulation.” Accordingly, the Tax Court’s reliance on State Farm and the cases following it was a “key misstep” by the Tax Court.

The Harvey Group also proposes that, should the Ninth Circuit find that the term “arm’s length standard” or the meaning of the “coordinating regulations” is ambiguous, the government’s interpretation embodied in Treas. Reg. § 1.482-7 should be afforded Auer deference. Read more on deference principles in tax cases and the unique challenges of Auer deference.Auer deference is a special level of deference that can apply when an agency interprets its own regulations, although there are several limitations on its use. Finally, if the Ninth Circuit decides that the regulations “have an infirmity,” the Harvey Group argues that “[t]he best remedy is to remand to Treasury for further consideration.”

A second group of nineteen professors (Alstott Group) similarly agrees with the government’s arguments to the Ninth Circuit. The Alstott Group argues that the 1986 addition of the “commensurate with income” standard [...]

Subscribe

Subscribe

")