Taxpayers are running out of time to file refund claims against the government. If the government reduced or denied your Section 1603 cash grant, you can file suit in the Court of Federal Claims against the government to reclaim your lost grant money. Don’t worry, you will not be alone. There are numerous taxpayers lining up actions against the government and seeking refunds from this mismanaged renewable energy incentive program. Indeed, the government lost in round one of Alta Wind I Owner-Lessor C. v. United States, 128 Fed. Cl. 702 (2016). In that case, the trial court awarded the plaintiffs more than $206 million in damages ruling that the government unreasonably reduced their Section 1603 cash grants.

The October 2017 issue of Focus on Tax Strategies & Developments has been published.This issue includes five articles that provide insight into US federal and international tax developments and trends across a range of industries, as well as strategies for navigating these complex issues.

The White House and Republican congressional leadership released an outline this week to guide forthcoming legislation on tax reform. This outline will serve as a useful framework in structuring what will be an active, and likely contentious, phase of reform activity.

The Internal Revenue Service (IRS) and taxpayers frequently spar over the meaning and interpretation of tax statutes (and regulations). In some situations, one side will argue that the statutory text is clear while the other argues that it is not and that other evidence of Congress’ intent must be examined. Courts are often tasked with determining which side’s interpretation is correct, which is not always an easy task. This can be particularly difficult where the plain language of the statute dictates a result that may seem unfair or at odds with a court’s views as the proper result.

The Tax Court’s (Tax Court) recent opinion in Borenstein v. Commissioner, 149 TC No. 10 (August 30, 2017), discussed the standards to be applied in interpreting a statute and reinforces that the plain meaning of the language used by Congress should be followed absent an interpretation that would produce an absurd result.

In Borenstein, the taxpayer made tax payments for 2012 totaling $112,000, which were deemed made on April 15, 2013. However, she failed to file a timely return for that year and the IRS issued a notice of deficiency. Before filing a petition with the Tax Court, the taxpayer submitted return reporting a tax lability of $79,559. The parties agreed that this liability amount was correct and that the taxpayer had an overpayment of $32,441 due to the prior payments. However, the IRS argued that the taxpayer was not entitled to a credit or refund of the overpayment because, under the plain language of Internal Revenue Code Sections 6511(a) and (b)(2)(B), the tax payments were made outside the applicable “lookback” period keyed to the date the notice of deficiency was mailed. (more…)

In a long-awaited decision, the US Tax Court recently held that gain realized by a foreign taxpayer on the sale of a partnership engaged in a US trade or business was a sale of a capital asset not subject to US tax, declining to follow Revenue Ruling 91-32. The government has yet to comment regarding its intentions to appeal.

In a highly-anticipated Technical Advice Memorandum (TAM) dated March 23, 2017 and released on July 21, 2017, the Internal Revenue Service (IRS) ruled that two taxpayers who had invested in a Limited Liability Company that owned and operated a refined coal facility (the LLC) were not entitled to refined coal production credits they had claimed because their investment in the LLC was structured “solely to facilitate the prohibited purchase of refined coal tax credits.” This analysis marks a departure from the position staked out by the IRS in a number of recent refined coal credit cases, which focused on whether taxpayers claiming refined coal credits were partners in a partnership that owned and operated a refined coal facility.

On June 20, 2017, the Internal Revenue Service (IRS) Large Business and International Division (LB&I) hosted its final webinar regarding LB&I Campaigns. Our previous coverage of LB&I Campaigns can be found here. The webinar focused on two campaigns: (1) Section 48C Energy Credits and (2) Land Developers – Completed Contract Method.

President Trump released his budget proposal for the 2018 FY on May 23, 2017, expanding on the budget blueprint he released in March. The budget proposal and blueprint reiterate the President’s tax reform proposals to lower the business tax rate and to eliminate special interest tax breaks. They also provide for significant changes in energy policy including: restarting the Yucca Mountain nuclear waste repository, reinstating collection of the Nuclear Waste Fund fee and eliminating DOE research and development programs.

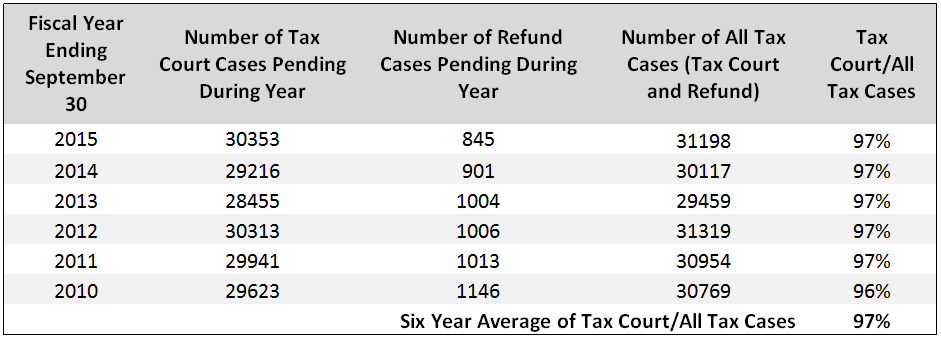

Taxpayers can choose whether to litigate tax disputes with the Internal Revenue Service (IRS) in the US Tax Court (Tax Court), federal district court or the Court of Federal Claims. Claims brought in federal district court and the Court of Federal Claims are tax refund litigation: the taxpayer must first pay the tax, file a claim for refund, and file a complaint against the United States if the claim is not allowed. Claims brought in the Tax Court are deficiency cases: the taxpayer can file a petition against the IRS Commissioner after receiving a notice of deficiency and does not need to pay the tax beforehand.

As demonstrated in the chart below, approximately 97 percent of tax claims are instituted in the Tax Court. It should be noted that, after a taxpayer files a petition in Tax Court, the taxpayer no longer has the option of bringing the claim in any other court for the year(s) at issue.

On April 5, 2017, in an unanimous court reviewed opinion, the United States Tax Court determined that disclosure of a worker’s tax return information to absolve the employer from liabilities arising out of the employer’s withholding requirement is not subject to the general prohibition against disclosing taxpayer return information pursuant to Internal Revenue Code (IRC) Section 6103, and does not shift the burden of proof to the Internal Revenue Service (IRS).

In Mescalero Apache Tribe v. Commissioner, 148 T.C. 11 (2017), the IRS determined that a number of the Mescalero Apache Tribe’s workers were not independent contractors, but employees. If the IRS prevailed in its worker reclassification determination then, as the employer, the Mescalero Apache Tribe would be jointly and severally liable for Federal income tax that should have been withheld on the workers’ earnings. To prevent double taxation, IRC Section 3402(d) provides that the IRS cannot collect from the employer the withholding tax liability if the employees have already paid income tax on their earnings. To prove its position that the workers were independent contractors and alternatively to reduce any potential withholding tax liability if the workers were classified as employees, the Mescalero Apache Tribe asked each worker to complete Form 4669, Statement of Payments Received. However, the Mescalero Apache Tribe had trouble locating each of its workers because many had moved or lived in hard-to-reach areas without phone service or basic utilities. (more…)

Subscribe

Subscribe

")