A frequently disputed tax issue is the proper treatment of costs incurred by taxpayers and whether they are currently deductible or must be capitalized. Internal Revenue Code (Code) Section 162 generally provides a deduction for ordinary and necessary business expenses paid or incurred during the taxable year in carrying on any trade or business. However, Code Section 263 provides no deduction for any amount paid for permanent improvements made to increase the value of any property. Code Section 263 requires capitalization of, amongst other things, costs paid or incurred to facilitate the acquisition of a trade or business. The capitalization rules of Code Section 263 trump the deductibility rules of Code Section 162. (more…)

Internal Revenue Code Section 199 permits taxpayers to claim a 9 percent deduction related to the costs to develop software within the U.S. The relevant regulations and their interpretation, however, place substantial restrictions on claiming the benefit.

Moreover, the regulations and the government’s position haven’t kept up with the technological advances in computer software.

Before claiming the deduction on your return, consider that the Internal Revenue Service has this issue within its sights, and perhaps it will be the subject of one of their new “campaigns.”

In 2004, Congress enacted I.R.C. Section 199 to tip the scales of global competitiveness more in favor of American business. The main motivation of the statute was to create jobs by encouraging businesses to manufacture and produce their products in the U.S. The tax benefit, however, isn’t available for services, a theme that pervades many of the provisions in the statute and regulations.

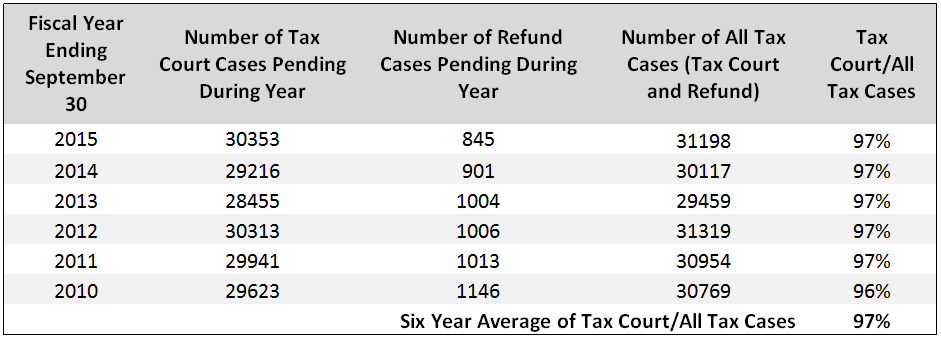

Taxpayers can choose whether to litigate tax disputes with the Internal Revenue Service (IRS) in the US Tax Court (Tax Court), federal district court or the Court of Federal Claims. Claims brought in federal district court and the Court of Federal Claims are tax refund litigation: the taxpayer must first pay the tax, file a claim for refund, and file a complaint against the United States if the claim is not allowed. Claims brought in the Tax Court are deficiency cases: the taxpayer can file a petition against the IRS Commissioner after receiving a notice of deficiency and does not need to pay the tax beforehand.

As demonstrated in the chart below, approximately 97 percent of tax claims are instituted in the Tax Court. It should be noted that, after a taxpayer files a petition in Tax Court, the taxpayer no longer has the option of bringing the claim in any other court for the year(s) at issue.

On April 4, 2017, QinetiQ U.S. Holdings, Inc. petitioned the US Supreme Court to review the US Court of Appeals for the Fourth Circuit’s decision that the Administrative Procedure Act of 1946 (APA) does not apply to the Internal Revenue Service (IRS) Notices of Deficiency. We previously wrote about the case (QinetiQ U.S. Holdings, Inc. v. Commissioner, No. 15-2192) here, here, here and here. To refresh, the taxpayer had argued in the US Tax Court that the Notice of Deficiency issued by the IRS, which contained a one-sentence reason for the deficiency determination, violated the APA because it was “arbitrary, capricious, an abuse of discretion, or otherwise not in accordance with law.” The APA provides a general rule that a reviewing court that is subject to the APA must hold unlawful and set aside an agency action unwarranted by the facts to the extent the facts are subject to trial de novo by the reviewing court. The Tax Court disagreed, emphasizing that it was well settled that the court is not subject to the APA and holding that the Notice of Deficiency adequately notified the taxpayer that a deficiency had been determined under relevant case law. The taxpayer appealed to the 4th Circuit, which ultimately affirmed the Tax Court’s decision. (more…)

On March 28, 2017, EY and the Internal Revenue Service (IRS) held a joint webcast presenting the Large Business & International’s (LB&I) new “Campaign” examination process. This was the IRS’s second in a planned eight-part series about Campaigns. The IRS speakers for the presentation were Tina Meaux (Assistant Deputy Commissioner Compliance Integration) and Kathy Robbins (Enterprise Activity Practice Area). We previously blogged about Campaigns on February 1, 2017 (link), and the first Campaigns webinar on March 8, 2017 (link).

The Acting Chief Counsel announced that effective April 1, 2017, Drita Tonuzi will serve as the Deputy Chief Counsel (Operations), in Washington DC. In this position, Ms. Tonuzi will provide legal guidance and litigation support to the Internal Revenue Service (IRS) and the Departments of Treasury and Justice in all matters pertaining to the administration and enforcement of the Internal Revenue laws. This includes responsibility for all litigation in the United States Tax Court as well as the management of personnel in fifty field offices nationwide and in headquarters operations in Washington, DC. She will directly supervises nine Divisions including Large Business and International (LB&I), Small Business/Self Employed (SB/SE), Tax Exempt and Governmental Entities (TEGEDC), Wage and Investment (W&I), General Legal Services (GLS), Criminal Tax (CT), Procedure and Administration (P&A), Finance and Management (F&M) and Counsel to the National Taxpayer Advocate (CNTA).

Ms. Tonuzi began her career with the Office of Chief Counsel in 1987 in the Manhattan Office, where she litigated cases before the United States Tax Court. She served as the Securities & Financial Services Firms Industry Counsel and managed a group of attorneys, Deputy Division Counsel for the Large Business & International Division (formerly LMSB), where she was responsible for the operation and litigation of the organization and most recently she served as Associate Chief Counsel Practice and Administration.

With Ms. Tonuzi’s promotion, Kathryn Zuba has been appointed as the Acting Associate Chief Counsel, Procedure and Administration. Ms. Zuba will head an office of more than 150 professionals, who provide legal services to the IRS, other components of the Chief Counsel’s Office, other government agencies, and the public in the areas of federal tax procedure and administration. The responsibilities of this office include matters relating to the reporting and payment of taxes; assessment and collection of taxes; the abatement, credit or refund of over-assessments or overpayments of taxes; the filing of information returns; bankruptcy; disclosure; FOIA; privacy law; litigation sanctions; judicial doctrines; ethics; and liaison with the courts.

On March 13 and 14, the 2nd International Conference on Taxpayer Rights was held in Vienna, Austria. More than 150 individuals from more than 40 countries attended the conference, which connects government official, scholars and practitioners from around the world to explore how taxpayer rights globally serve as the foundation for effective tax administration. This is the first of two posts recapping the issues discussed at the conference.

Four panels were held on March 13: (1) The Framework and Justification for Taxpayer Rights; (2) Privacy and Transparency; (3) Protection of Taxpayer Rights in Multi-Jurisdictional Disputes; and (4) Access to Rights: the Right to Quality Service in an Era of Reduced Agency Budgets.

Today, the Internal Revenue Service (IRS) released Revenue Procedure 2017-25 extending the Fast Track Settlement (FTS) program to Small Business / Self Employed (SB/SE) taxpayers. The IRS’s SB/SE group serves individuals filing Form 1040 (US Individual Income Tax Return), Schedules C, E, F or Form 2106 (Employee Business Expenses), and businesses with assets under $10 million.

FTS offers a customer-driven approach to resolving tax disputes at the earliest possible stage in the examination process. The program provides an independent IRS Appeals review of the dispute. Under this approach, the IRS Appeals Officer acts as the mediator and has settlement authority.

The purpose of the program is to reduce the time to resolve cases and to provide the IRS Exam Team with the authority to settle cases based on hazards of litigation (which is generally reserved for IRS Appeals Officers). FTS has been considered a great success by the IRS and many taxpayers. The expansion of this successful alternative dispute resolution makes sense in light of the ever-shrinking resources of the IRS.

Two petitions for certiorari pending before the Supreme Court of the United States ask the Court to resolve the question of whether a tax return filed after an assessment by the Internal Revenue Service (IRS) is a “return” for purposes of the Bankruptcy Code (BC). The answer to this question will determine whether a bankrupt taxpayer’s tax debts can be discharged or are permanently barred from discharge. According to these petitions, the courts of appeal are divided as to the answer.

BC § 523(a) generally allows a debtor to discharge unsecured debt, except for, inter alia, tax debts of debtors who: (1) failed to file tax returns; (2) filed fraudulent tax returns; or (3) filed late tax returns, where a bankruptcy petition is filed within two years of the date the late return was filed. See BC § 523(a)(1)(B)(i), (B)(ii), (C).

On January 31, the Internal Revenue Service (IRS) announced 13 Large Business & International (LB&I) “campaigns.” One campaign targets deductions claimed by multi-channel video programming distributors (MVPDs) and TV broadcasters under section 199 of the Internal Revenue Code (IRC). According to the IRS’s campaign announcement, these taxpayers make several erroneous claims, including that (1) groups of channels or programs constitute “qualified films” eligible for the section 199 domestic production activities deduction, and (2) MVPDs and TV broadcasters are producers of a qualified film when they distribute channels and subscription packages that include third-party content.

IRC section 199(a) provides for a deduction equal to 9 percent of the lesser of a taxpayer’s “qualified production activities income” (QPAI) for a taxable year and its taxable income for that year. A taxpayer’s QPAI is the excess of its “domestic production gross receipts” (DPGR) over the sum of the cost of goods sold and other expenses, losses or deductions allocable to such receipts. IRC section 199(c)(1). DPGR includes gross receipts of the taxpayer which are derived from any lease, rental, license, sale, exchange, or other disposition of “any qualified film produced by the taxpayer.” IRC section 199(c)(4)(A)(i)(II). A “qualified film” is “any property described in section 168(f)(3) if not less than 50 percent of the total compensation relating to the production of such property is compensation for services performed in the United States by actors, production personnel, directors and producers.” IRC section 199(c)(6). However, “qualified film” does not include property with respect to which records are required to be maintained under 18 U.S.C. § 2257 (i.e., sexually explicit materials). Id. Under regulations issued in 2006, “qualified film” also includes “live or delayed television programming.” Treas. Reg. § 1.199-3(k)(1); see also Notice 2005-14, 2005-1 C.B. 498, §§ 3.04(9)(a), 4.04(9)(a). “Qualified film” includes “any copyrights, trademarks, or other intangibles with respect to such film.” IRC section 199(c)(6). The “methods and means of distributing a qualified film” have no effect on the availability of the section 199 deduction. Id. IRC section 168(f)(3), entitled “Films and Video Tape,” provides an exclusion from accelerated depreciation for “[a]ny motion picture film or video tape.”

Though the January 31 announcement did not explain the IRS’s position on these issues in detail, the IRS rejected both claims in two Technical Advice Memoranda (TAMs) issued in late 2016. The IRS determined in TAM 201646004 (Nov.10, 2016) and TAM 201647007 (Nov.18, 2016) (the 2016 TAMs) that a subscription package of multiple channels of video programming transmitted by an MVPD to its customers via signal is not a “qualified film” as defined in IRC section 199(c)(6) and Treas. Reg. § 1.199-3(k)(1). It also determined that an MVPD’s gross receipts from its subscription package are not from the disposition of a qualified film produced by the MVPD and are therefore not DPRG included in calculating a section 199 deduction. The MVPD would only have DPRG from the subscription package to the extent its gross receipts are derived from an individual film or episode within the subscription [...]

Subscribe

Subscribe

")