Subscribe

SubscribeCheck out our summary of significant Internal Revenue Service (IRS) guidance and relevant tax matters for March 9, 2026 – March 25, 2026.

AI controversy developments

March 20, 2026: The US Tax Court is considering developing a disciplinary framework for the misuse of artificial intelligence (AI) in litigation following concerns raised by Judge Mark V. Holmes regarding lawyers citing AI-generated, nonexistent cases. Judge Holmes indicated that the Court is proceeding cautiously given that a large share of its docket involves pro se taxpayers and emphasized the difficulty of crafting appropriate sanctions in that context. The discussion highlights broader concerns about hallucinated authorities, potential IRS misuse of AI, and the need to protect sensitive taxpayer information as the Court balances enforcement with legitimate AI uses.

IRS guidance

March 13, 2026: The IRS announced that the secretary of the US Department of the Treasury is no longer serving as acting IRS commissioner following the expiration of authority under the Federal Vacancies Reform Act of 1998. Chief Executive Officer Frank J. Bisignano is currently leading the IRS’s day-to-day operations.

March 16, 2026: The IRS issued Revenue Ruling 2026-11, updating the rules and technical specifications for substitute versions of Form 941, Form 8974, and related schedules, including Schedules B, D, and R. The guidance provides standards for paper and computer-generated substitutes used by software developers and payroll providers and supersedes prior guidance.

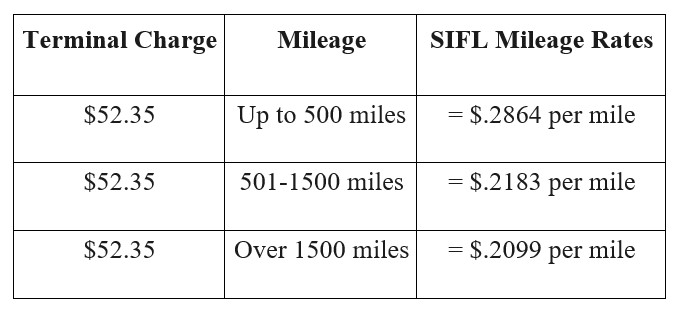

March 17, 2026: The IRS issued Notice 2026-19, providing updated interest rates for pension the corporate bond monthly yield curve, spot segment rates under Internal Revenue Code (Code) § 417(e)(3), and 24-month average segment rates under Code § 430(h)(2). The notice also includes the applicable 30-year Treasury rate for February 2026 (4.76%) and related weighted average rates.

March 18, 2026: The IRS issued Notice 2026-20, extending for one additional year the temporary relief provided by Notice 2025-7, which allows taxpayers to use alternative methods to identify which units of digital assets are sold, disposed of, or transferred when held with a broker. Under this relief, taxpayers may identify units on their own books and records, including through standing orders, rather than communicating with brokers. The notice clarifies that this does not prevent taxpayers from complying with § 1.1012-1(j)(3)(ii).

March 20, 2026: The IRS issued Revenue Procedure 2026-17, providing transition relief under Code § 163(j) that allows certain taxpayers to withdraw previously irrevocable elections to be treated as electing real property trades or businesses, electing farming businesses, or excepted regulated utility trades or businesses. The guidance also permits taxpayers withdrawing those elections to make a late election out of bonus depreciation, allows taxpayers to revoke or make controlled foreign corporation group elections without regard to the 60-month limitation, and permits eligible Bipartisan Budget Act of 2015 (BBA) partnerships to file amended Forms 1065 and issue amended Schedules K-1.

The IRS also released its weekly list of written determinations (e.g., Private Letter Rulings, Technical Advice Memorandums, and Chief Counsel Advice).

Recent court decisions

March 9, 2026: [...]

Continue Reading

read more

")